February 2025 Residential Transactions – Putterills Market Report

Overview: The UK housing market saw a surge in completed residential property transactions in February 2025, marking a robust start to the year.

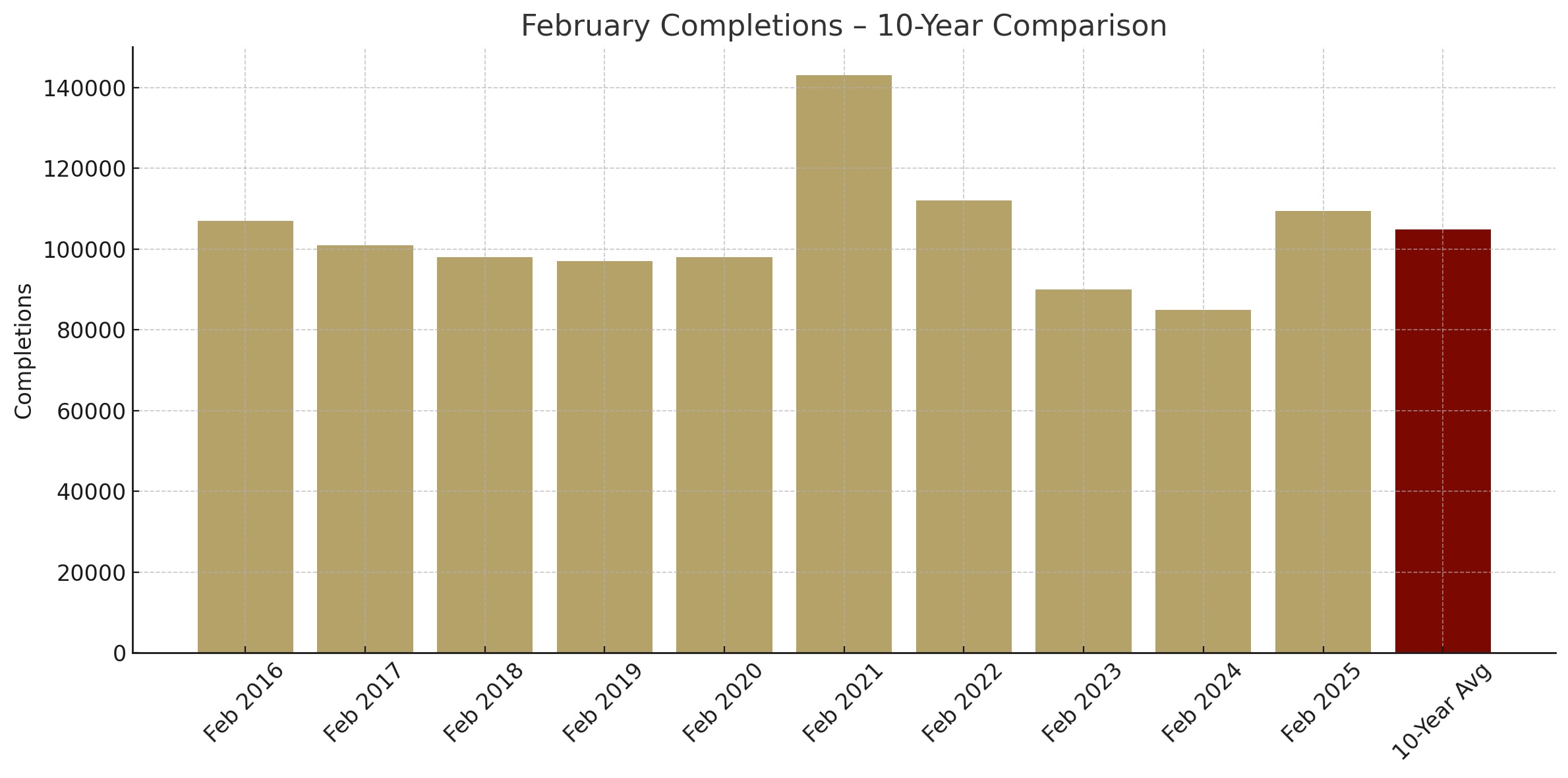

February 2025 in Context: A Decade-High Month

February 2025 stood out compared to the past decade, with transaction volumes surpassing every February in ten years. Completions this February were about 4.4% above the 10-year average. The only notable surge was in 2021 due to a temporary tax break, but 2025 has surpassed that. This performance shows market momentum is a sustained upward trend, not just a pandemic rebound. Increased buyer and seller activity made it one of the busiest Februaries on record, indicating a promising spring market for housing transactions.

February saw a strong increase following a healthy January, with a 13.8% rise in residential sales from January to February 2025. Approximately 108,000 sales were completed in February, up from around 95,000 in January. This sharp increase suggests many transactions were completed earlier, especially with the upcoming stamp duty deadline. Overall, February’s performance indicates sustained high buyer demand and a market exceeding long-term norms.

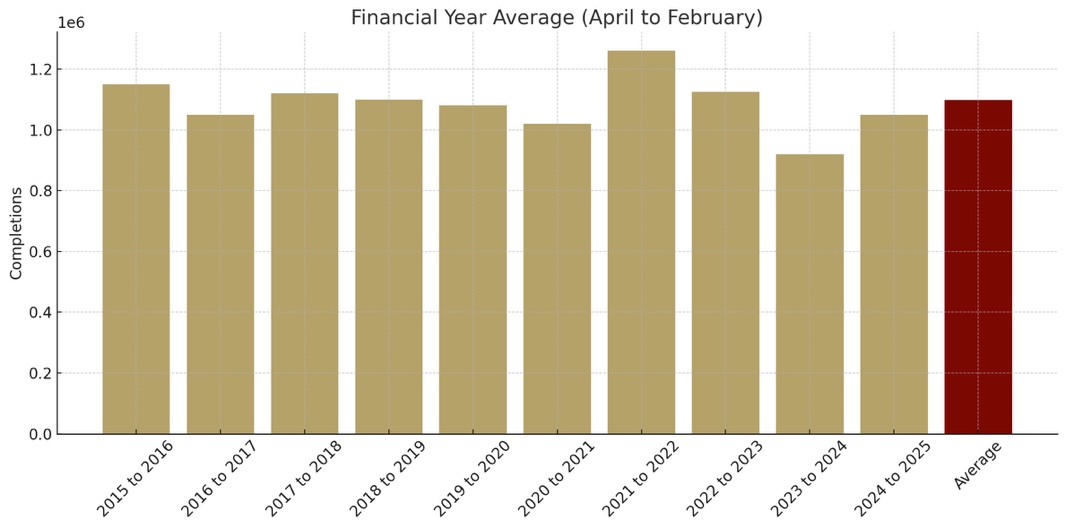

Financial Year-to-Date Performance (April–Feb)

When we take a step back and look at the financial year so far, we can see that the trend is looking quite positive! Figure 2 illustrates the completions from April to February for each year since 2015/16. For the current financial year 2024/25 (from April 2024 to February 2025), we're seeing transaction volumes that are 14.12% higher compared to the same period last year. In real terms, about 1.044 million residential sales have been completed so far this financial year, up from approximately 0.915 million at this time last year. This impressive increase shows that the market has bounced back from the slower activity we experienced in 2023. Furthermore, government data reveals that monthly transactions started to pick up in mid-2024 and continued to gain momentum into late 2024 and early 2025 – a trend that is clearly reflected in the figures we've seen so far this year!

It is worth noting that despite this year-on-year growth, the current April–Feb total is still around 4.65% below the 10-year average for the period. The red average bar in Figure 2 indicates that while 2024/25 has been strong, it has not fully reached the lofty transaction volumes seen when the market was at its peak (for example, during 2021’s post-lockdown boom).

Market context: the first half of the financial year (summer 2024) saw slightly muted activity due to higher interest rates and economic uncertainty, pulling the year-to-date average down slightly. However, the gap to the long-term average has been closing rapidly in recent months. Given the current trajectory, we expect the full 2024/25 year (ending March 2025) to come very close to the 10-year average, if not exceed it once March’s figures are in.

In summary, Putterills’ analysis of the financial year so far is optimistic. The uplift on last year’s performance is a clear indicator of market resilience. Even though volumes aren’t quite at the decade high watermark, the deficit has narrowed considerably. With one month left in the financial year, the market is positioned to finish strong, potentially surpassing historical norms if March’s activity comes in as expected.

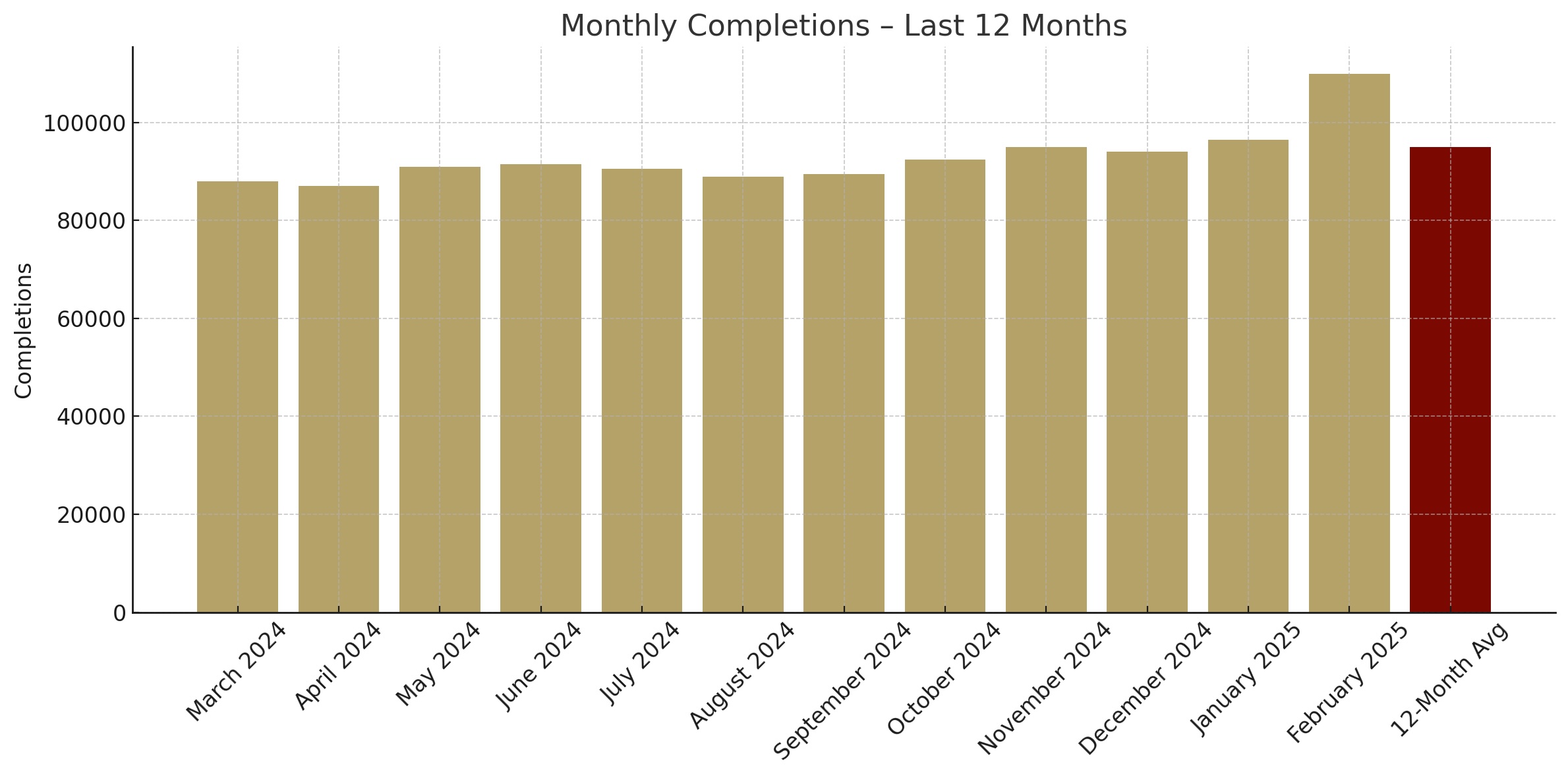

Monthly Trend and Moving Average

The the month-by-month trend from March 2024 to February 2025 illustrates the growing momentum. After a dip in mid-2024, completions steadily increased toward year-end. By autumn 2024, the market gained traction, with October and November achieving 95–105k transactions (seasonally adjusted), surpassing the summer lull. Although December saw a seasonal dip, levels stayed above last summer's figures.

Due to the late-year recovery, the 12-month average is now about 93,500 transactions per month. February 2025’s completion count is around 15.8% higher than the previous year's average, marking it as the strongest month in this period. This shows that transaction pace has accelerated, raising the average.

January and February 2025 show a clear spike. January’s completions were about 10% above the 12-month average, and February increased this further. This surge is partly due to buyers completing purchases before the 31 March 2025 stamp duty deadline. Some activity likely spread to March or April was brought forward to these winter months. Still, the underlying trend is positive: every month since September 2024 has exceeded the 12-month moving average, indicating growth in housing market activity.

What’s Driving the Surge?

Several factors are driving the strong market:

• Stamp Duty Deadline: The imminent change to Stamp Duty Land Tax rates on 1 April 2025 is pushing buyers to complete transactions early. The nil-rate band for standard purchases will halve from £250,000 to £125,000, and first-time buyer relief thresholds will also decrease. This created urgency, pulling many completions into Jan/Feb. Data indicates a forestalling effect, with transactions rushed to save on tax.

Putterills agents noted a surge in conveyancing and mortgage finalisations.

• Interest Rate Stabilisation: After hikes in 2022 and 2023, mortgage rates have steadied, enhancing buyer confidence and affordability. By late 2024, more buyers returned with clearer borrowing costs, increasing transactions.

Improved Supply: An increase in property listings compared to the tight supply of 2021–2022 has facilitated more successful transactions. Putterills saw greater stock availability in popular segments, enabling higher sales volume.

Underlying Demand: Despite economic challenges, demand for housing remains robust, driven by demographic factors and relocation interests, keeping buyers active even amidst price fluctuations. Financing is available at historically reasonable rates.

Market Outlook Post-Deadline

Post-March, Putterills is optimistic for the market:

Robust Momentum: The market enters Q2 2025 with significant momentum. Even with a slight cooling in April, activity levels are expected to remain healthy, with many deals in progress unrelated to the stamp duty rush.

Spring Selling Season: Typically, spring is the busiest property season. We expect an uptick in new listings and inquiries in April and May, offsetting any decline from the tax break's ending. Early indicators show rising market valuations and fresh supply.

Economic Factors: The economic backdrop is stable. Inflation is under control, and interest rates may peak, potentially easing mortgage rates by late 2025, which would improve buyer affordability. High employment in key areas supports buyers' purchasing decisions.

Buyer Sentiment: The stamp duty deadline increased urgency but highlighted pent-up demand. Those who missed the deadline still need to move, and improving mortgage options will assist first-time buyers. Any April dip is likely temporary, as the market should stabilize in summer at or above long-term transaction averages.

Conclusion: The data reflects a resilient property market. February 2025’s performance underscores robust demand despite policy changes. Although some activity was deadline-driven, the overall trend indicates recovery and growth. Putterills is encouraged by the figures, indicating a market rebounding and exceeding expectations. Confident of steady transaction volumes through spring and summer 2025, we anticipate ongoing strength in the housing market, with high demand for sellers and an active environment for buyers. Overall, indicators point to a strong remainder of 2025 for UK residential transactions, with Putterills ready to assist clients in navigating this dynamic marketplace.