Our comprehensive budget review follows the second base rate reduction this year.

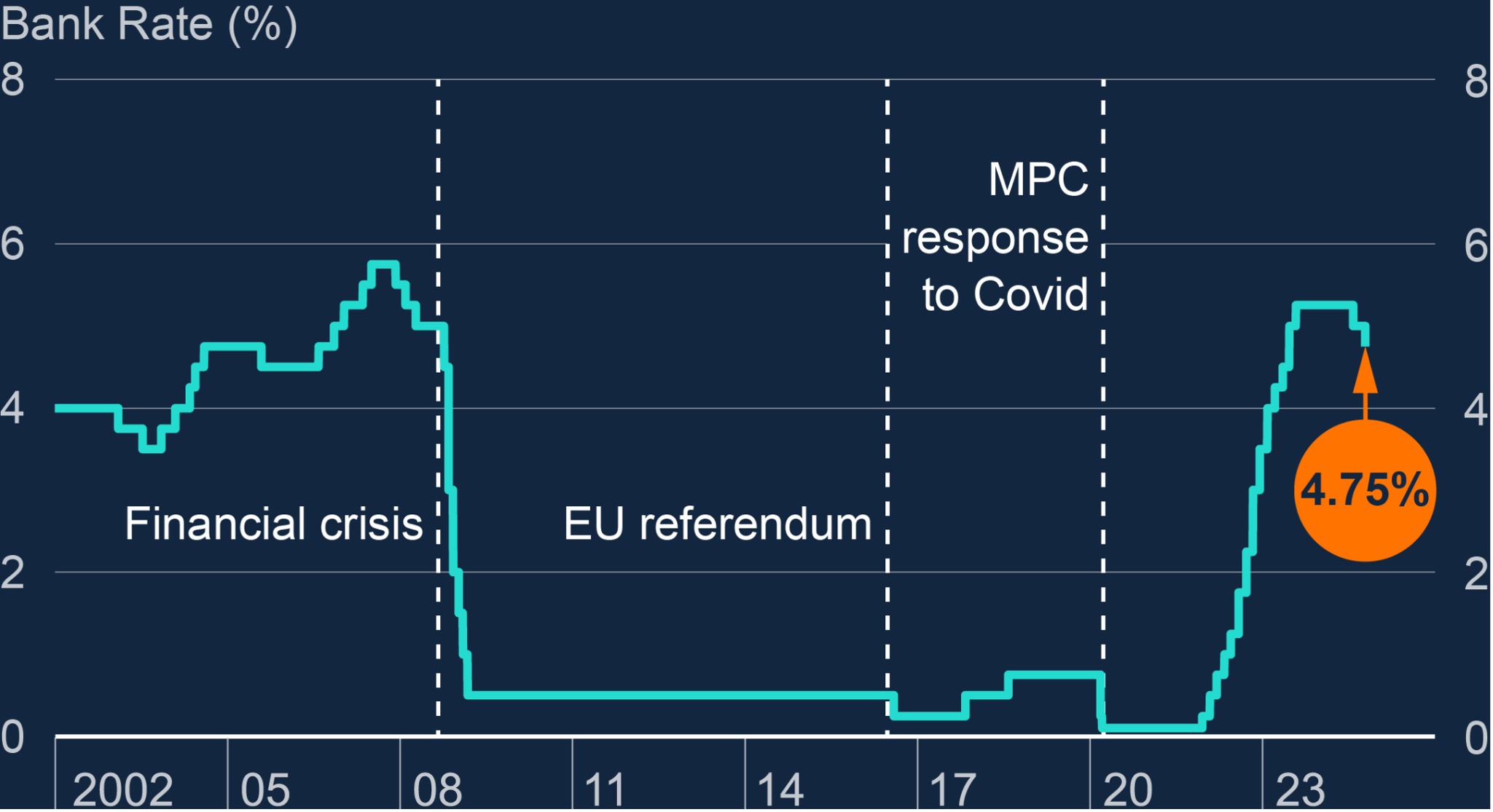

The Bank of England has announced its second Base Rate reduction of the year, dropping from 5% to 4.75%.

Base rate cut to 4.75%

This outcome was widely expected by the financial markets, but the decision saw all but one of the committee members vote to reduce the Base Rate to its lowest level since May 2023.

This indicates much wider support for this move compared to the 5-4 vote split for the first rate cut in August.

The last meeting in September also saw the MPC vote overwhelmingly in favour of keeping the Base Rate unchanged at 5%, with all but one of the nine-strong committee supporting the decision to pause. This is perhaps a sign that the majority supports a quarterly cutting cycle.

This Base Rate decision follows a run of important economic and political events, including the budget and the US election.

This has resulted in a view that the Base Rate will be cut at a more moderate pace than previously expected and has been priced in by lenders.

Therefore, we are likely to see average mortgage rates drift up a little in the short term before starting to fall back again.

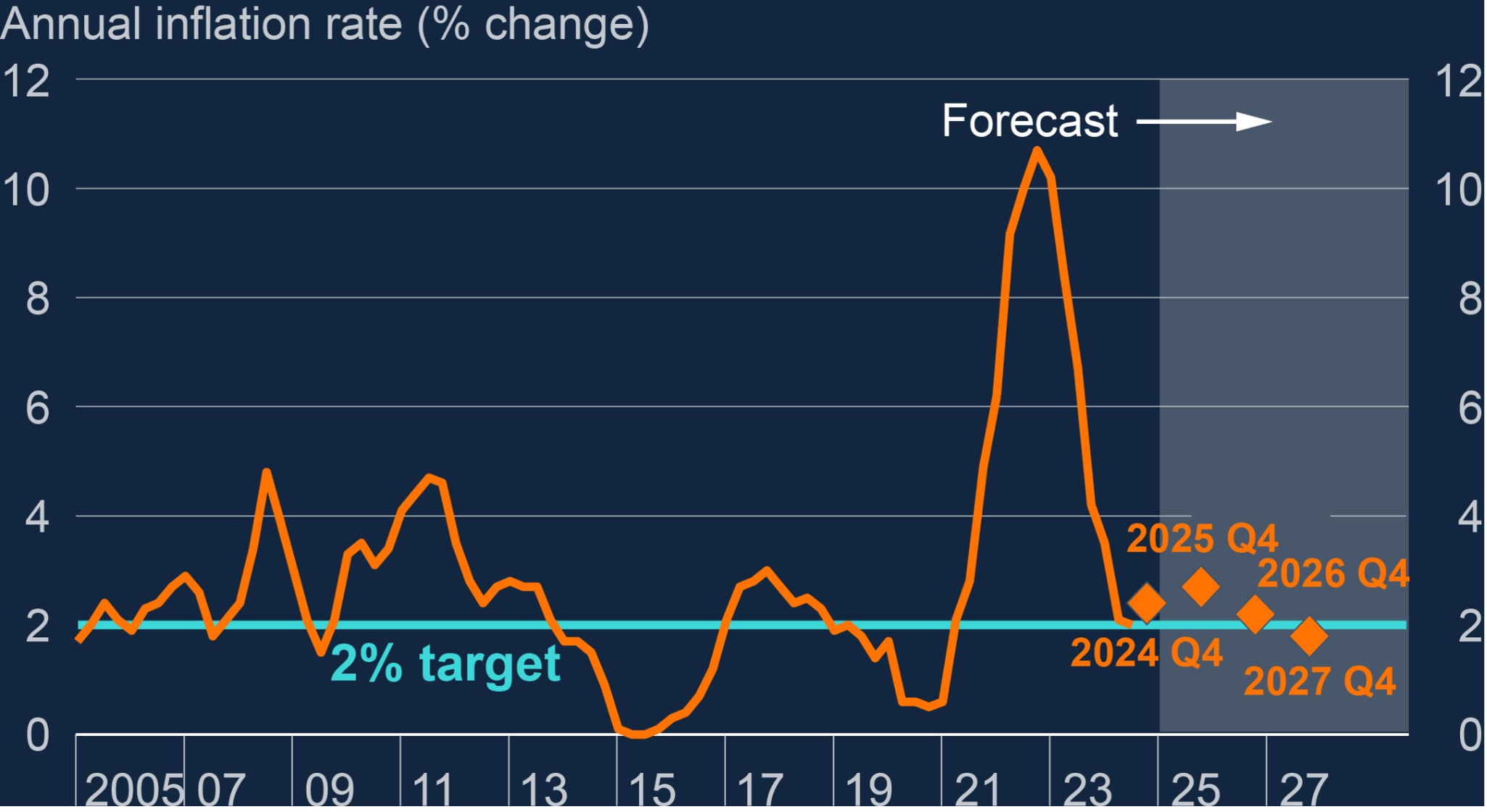

Updated economic projections from the BoE presented in the latest quarterly Monetary Policy Report supported this cautious message.

From a current rate of 1.7%, inflation is expected to rise to 2.5% by the end of the year and climb further over 2025 before peaking around 2.8% in Q3.

With this in mind, the markets have reduced the probability of a rate cut in December to just 25%, down from 35-40%, with a 0.25% reduction by February almost fully priced in.

What’s happened to mortgage rates recently?

Some lenders have been increasing their rates in recent weeks, whilst others have been reducing them as there has been a lot of movement in swap rates, which has meant lenders have needed to reprice their mortgage products back in line with the rest of the mortgage market.

The average rate for a five-year fixed-rate mortgage on 7 November 2024 is 4.7%, up from 4.64% the week before.

The average rate for a two-year fixed-rate mortgage is 4.95%, up from 4.91% the week before.

The lowest available 5-year fixed rate mortgage is 3.84%, and the lowest available two-year fixed rate is 3.96%, both unchanged from last week.

Whilst a drop in the base rate won’t significantly impact interest rates immediately as you can see from the figures above, particularly with the reaction to the swap and gilt rates following the budget, it should follow suit of the positive reaction to the 0.25% cut at the start of August and help expedite movement in the market.

The decline in the base rate had already been factored into lower mortgage rates, which reached a two-year low over the autumn. This has definitely helped bring a return of buyer activity to the market.

Given the outlook for the base rate, many predict that the current average rate of 4-5% will remain throughout 2025.

The Office for Budget Responsibility recently released its economic and fiscal outlook, which sets out its central forecast for the next five years, taking into account recent data and government policies.

They reported that average interest rates on the stock of mortgages are expected to rise from around 3.7% in 2024 to a peak of 4.5% in 2027, then remain around that level until the end of the forecast.

The high proportion of fixed-rate mortgages (around 85%) means increases in Bank Rate feed through slowly to the stock of mortgages.

Bank of England analysis shows around two-thirds of fixed-rate mortgages have been repriced since the start of this hiking cycle, and UK Finance analysis shows that around 1.8 million will end next year.

What could lie ahead for interest rates?

Goldman Sachs recently predicted that the base rate could fall to 2.75% by next November, although this prediction is more ambitious than other previous ones. The International Monetary Fund suggested in May that the base rate could drop to 3.5% by the end of 2025, and Capital Economics reported in July that they expect the base rate to hit 3% by the end of next year.

Below are the latest forecasts from Savills residential research arm for what they believe is in store for interest rates, the property market and the economy over the next five years.

As you can see from the above they forecast, are predicting a gradual improvement in conditions and this stability should see more people enter the market as they feel comfortable in their moving decision.

The bounceback in activity for new listings, sales agreed, and house price growth in 2024 is evidence that interest rates averaging 4-5% can 100% support the market. If conditions improve further, slowly but surely, the market will react positively to this despite continuous political and economic uncertainty.

Therefore, we should expect a continued but steady upward trajectory for transaction levels and house prices.

Reaction to the budget

On 30 October, the nation saw the much-anticipated first budget from a Labour government since 2010.

The property market reacted with an initial slight panic to immediate changes in Stamp Duty for purchasing additional homes, which saw it increase from 3% to 5% as of 31 October.

According to Nationwide, based on data for the year ending June 2024, this change would affect approximately 20% of transactions.

There were also no mentions of any extensions or changes to existing stamp duty thresholds for those buying the only residential property they own or if they are buying their first home.

Therefore, as of 1 April 2025, paying stamp duty for those who have owned a home before and are buying their only residential property will go from paying nothing up to £250,000 to starting paying 2% from £125,001 to £250,000.

For first-time buyers the amount in which they are not liable for stamp duty will reduce from £425,000 to £300,000 and 5% on the portion from £300,001 to £500,000, down from £525,001 to £625,000.

If the price is above £500,000, a first-time buyer will not be able to claim any relief.

Consequently, this could arguably dampen demand in the market causing transaction levels to drop and house prices to decrease, but is that going to be the case.....

What’s next?

The uncertainty of the budget is behind us, a cut to the base rate has happened and we have stamp duty reverting back to where it was in 2022 at the start of April.

Therefore, we expect to see an increase in transaction levels between now and the end of March as buyers aim to take advantage of the current stamp duty thresholds before the end of March deadline.

Anyone considering taking advantage of the current situation should act sooner rather than later as it is currently taking an average of 213 days from listing a property to completing a transaction according to Rightmove.

Many people can be put off listing their home in the winter months now that the days are shorter, but with the right pricing and marketing strategy in place, there is 100% pent-up demand out there that sellers can tap into and help get moved ahead of schedule.

I hope you enjoyed reading my reaction to yesterday's news. If you need any support buying, selling or renting property, please reach out to a member of the Putterills Team.